Buy-side calibrated.

Five years inside an investment holding company, on the buy side of the capital that acquires firms like yours. The read reflects how acquirers actually price - not how a seller's agent hopes they will.

For owner-operated firms · mid-market

Private equity already bought the big players. Now it's coming down-market - for firms like yours. The range your industry hands you isn't fixed; it's a starting point. We diagnose where you stand, quantify what's discounting you, and map the moves that reposition you into a higher-multiple peer group — moves you own and run on your own timeline. Buy-side calibrated. No success fees, no retainer.

Market intensity · 2024–2025

PitchBook via Capstone / CapitalPad, FY2024 (4,908 bolt-ons tracked).

S&P Global, mid-2025 (~$2.5T global private capital dry powder).

Capstone Partners, fragmented-services roll-up tracking, 2024.

J.P. Morgan Asset Management, lower-middle-market deal data, 2024.

The wave

How a private-equity roll-up changes your valuation multiple

Industry after industry runs the same arc. The wave reaches the owner-operated tier last - and that's where the choice still exists. Wait too long and the platform on-ramp closes: you can only be acquired, not the one doing the acquiring.

How the consolidation wave reads, phase by phase. Every fragmented industry runs the same arc. In the Opening phase the top firms hold only low-single-digit market share and there are few institutional platforms — multiples are low and flat. In Acceleration, private-equity platforms multiply and add-on activity rises, bidding entry multiples up and widening the gap between a small firm and a scaled platform. At the Peak — the window — the most platforms are competing at once and the scale premium is widest. The Late phase arrives once the prime assets are absorbed: platform-on-platform mergers dominate, and the premium concentrates in a few integrated leaders while later, lower-quality sellers meet softer terms.

The single signal that settles where a sector sits is the PE-to-PE flip — the moment one private-equity owner sells a platform to another at a step-up. It means the easy fragmentation is gone and the sector is at or past its peak. It already happened in accounting: New Mountain Capital backed Citrin Cooperman at roughly 11× EBITDA in 2022, and Blackstone acquired that stake at about 15× in January 2025 — the first such flip of a top US CPA firm. (Sources: Blackstone / PR Newswire, Jan 7 2025; CPA Practice Advisor.)

Chart is illustrative and directional — individual sectors sit at different points, and the "today" position is a generalization, not a forecast for any one firm. See the live worked example on our architecture & engineering vertical.

Accounting

First PE-to-PE platform flip already happened — the late-cycle tell.

Veterinary

Group ownership past a third of clinics; secondary sponsor trades dominate.

IT managed services (MSPs)

Wave 2 closing; recurring-revenue books priced separately from break-fix.

Environmental

EPA PFAS super-wave + WSP–TRC at $3.3B reset the ceiling.

Architecture / engineering

552 firms changed hands last year; international buyers entering the US.

Behavioral health

Outpatient and ABA platforms scaling rapidly; the window is open and visibly closing.

Legal (MSO / ABS)

Arizona ABS + MSO structures are unlocking PE capital into law firms for the first time.

Cleaning / janitorial

Commercial janitorial contracts attractive; platform formation just beginning at scale.

Three decisions

Most owners answer them by default, not by design. Waiting doesn't just cost multiple - it deletes options, in order.

Passive default

Wait for inbound. Accept the window the market gives you.

Ambition

Move while the platform on-ramp is still open.

Timing is the master decision - it gates the other two.

Passive default

Be a tuck-in. Sell at the prevailing tuck-in multiple.

Ambition

Build the platform. Acquire and integrate the tuck-ins yourself.

Closes first when timing slips - you can no longer be the consolidator, only a target.

Passive default

Stay inside your industry's comp set. Accept its ceiling.

Ambition

Reposition into a higher-multiple peer group.

The repositioning runway shortens with the window.

Not every owner can or should become a platform - capital, appetite, and timeline all bear on it. The read identifies which path actually fits your situation.

A reframe

The multiple a buyer would pay today is the market's read on the quality of the asset you've already built - concentration, recurring revenue, owner dependency, leadership depth, backlog mix, the shape of growth. It's a grade, not a forecast.

Two firms with the same EBITDA and the same industry routinely land in very different places. The gap between them is rarely accident; it's the cumulative effect of a hundred small decisions made - or deferred - over the last five years. And the multiple is just as real if you never sell — if you're handing the firm to your kids, your partners, or a key employee.

The read tells you which decisions are quietly discounting you right now, and how many turns of EBITDA each one is worth.

The wedge

What drives your EBITDA multiple

The same business - same EBITDA, same people - is worth dramatically more as part of a scaled platform than as a small firm. That gap is what repositioning targets.

The same firm is worth dramatically more as a scaled platform than as a small business — that gap is what repositioning targets. Across mid-market service sectors, a typical small-firm EV/EBITDA range sits well below the range a scaled platform commands in the same sector. The spread widens as a sector moves through the consolidation wave: in peak-phase sectors the platform premium is at its largest.

Two concrete, confirmed reference points for how far the ceiling can sit above the floor: in environmental consulting, WSP's acquisition of TRC closed in February 2026 at US$3.3 billion — strategic-scale pricing driven by a regulatory super-wave (the EPA's 2024 PFAS drinking-water standards and CERCLA designation). In testing & inspection and accounting, scaled platforms trade in the low-to-mid-teens of EBITDA where independent firms trade in the mid-single digits. (Sources: WSP press release, Feb 24 2026; EPA PFAS rule, Apr 2024. Sector ranges are directional, advisor-reported 2024–26; verify against primary sources before relying on a specific figure.)

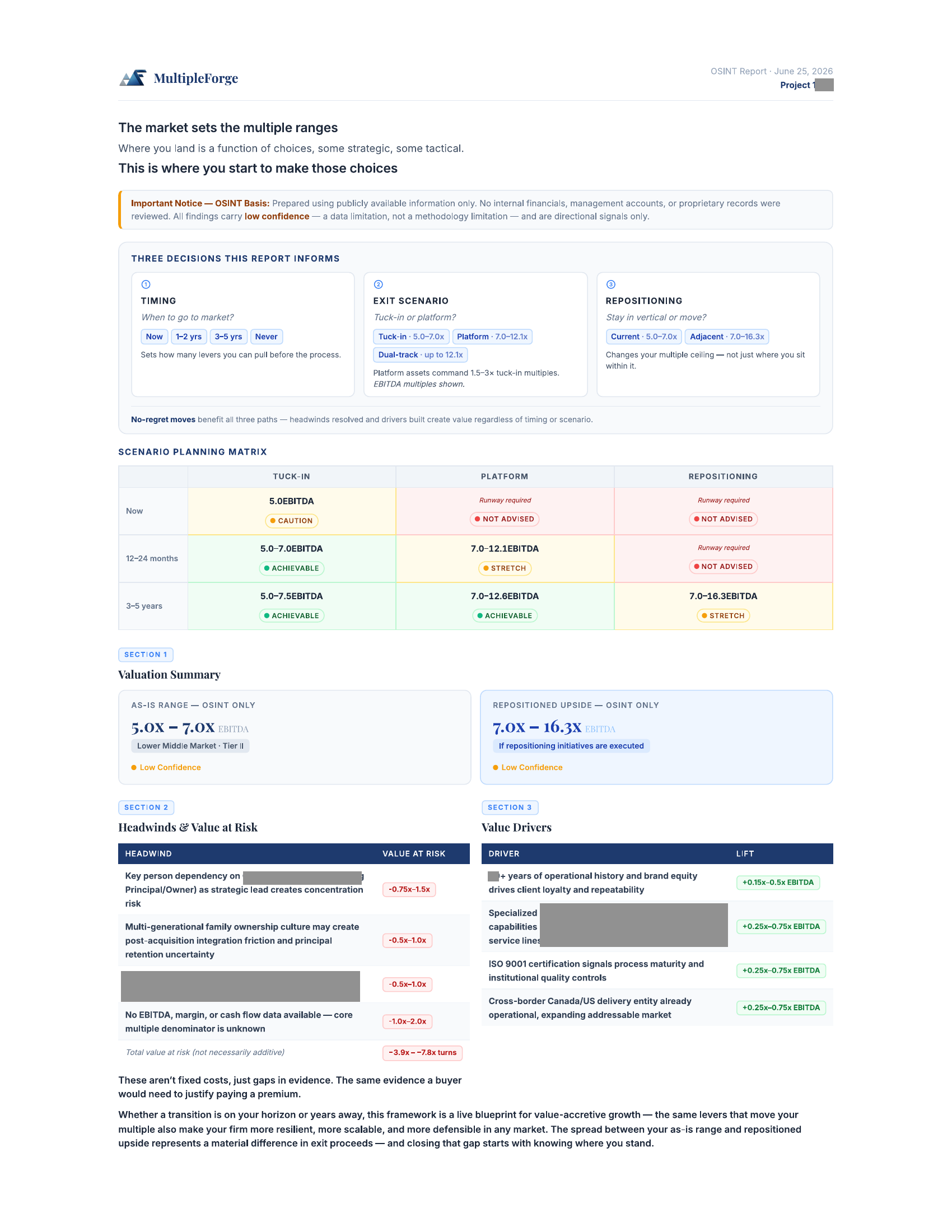

Sample · redacted

This is the shape of every complimentary read: a defensible starting multiple, every headwind quantified in turns of EBITDA, every driver mapped to a repositioned ceiling. Get a complimentary valuation read →

Why this is different

Five years inside an investment holding company, on the buy side of the capital that acquires firms like yours. The read reflects how acquirers actually price - not how a seller's agent hopes they will.

Four years at McKinsey & Company. The analytical discipline behind the diagnosis: structured, defensible, primary-sourced where it matters.

Almost two decades focused on owner-led services businesses. Pattern recognition is the unlock - and you don't get it from a framework, you get it from the reps.

Against the alternatives

Brokers & transaction advisors

Paid when a deal closes. Their read is event-driven and incentive-conflicted; they have no reason to actually improve the asset, only to move it.

Generalist consultants

Framework, but no capital-markets seat. They've never priced a firm as a buyer, so the multiple is theoretical.

Multiple Forge

Owner-aligned (no success fee), strategic (a live read you own and run yourself, not a standing engagement), buy-side-calibrated. A different thing.

What we are · what we're not

What we are

What we're not

Who this is for

The methodology is built for a specific kind of owner. Naming it up front saves us both time.

Fits

Doesn't fit

Soft ask · self-segment

Pick your industry. We'll route you to the right starting point - a vertical page where one exists, or directly into the complimentary read where it doesn't. Useful regardless of whether we ever talk.

opening

acceleration

peak

late

Acceleration · in the window · 9 industries

Pick a phase, then tap an industry to see where it sits — and one piece of evidence behind the placement.

Where these industries sit on the wave · illustrative, confirmed evidence where cited

Useful regardless · No success fees

FAQ · owners ask

It's the number a buyer multiplies your EBITDA by to price your firm — and it's not a fixed industry constant. It's the market's read on the quality of what you've built: customer concentration, how much recurring revenue you carry, how dependent the business is on the owner, the depth of your leadership bench, backlog mix, and the shape of your growth. Two firms with identical EBITDA in the same industry routinely sell at very different multiples. The gap is the cumulative result of a hundred decisions made or deferred over five years.

Two moves, in order. First, remove what's quietly discounting you — the headwinds a buyer would point to (client concentration, owner-dependent business development, a thin layer below the founder, no recurring revenue). Each one is worth a measurable number of turns of EBITDA. Second — the bigger move — reposition into a higher-multiple peer group, so the market compares you to a different, better-priced universe of firms. The first move recovers value you're leaking; the second changes the ceiling entirely.

A roll-up is when private equity buys one "platform" firm and then acquires many smaller firms ("tuck-ins") to bolt onto it, building scale that commands a higher multiple than any single firm could. You're in one if the top players in your sector are being acquired, the number of PE-backed platforms is rising, and add-on deals are accelerating. The clearest tell is below.

It's the moment one private-equity owner sells a platform to another private-equity owner — usually at a higher multiple than they paid. It matters because it means the easy fragmentation is gone: there aren't enough independent firms left to keep building cheaply, so sponsors now trade platforms among themselves. When you see it, the sector is at or past its peak window. Accounting crossed that line when New Mountain's stake in Citrin Cooperman (bought at ~11× in 2022) was acquired by Blackstone at ~15× in January 2025 — the first such flip of a top US CPA firm.

They pay for different things. A strategic buyer pays for fit — what your firm adds to theirs (capabilities, geography, clients) — and can pay the highest number when the fit is strong. A PE platform pays for a scalable, de-risked asset it can grow and resell. The right answer depends on what you've built and what you want afterward; the worst answer is finding out which buyer you're built for only once you're in a process. A read tells you in advance which buyer would pay the premium, and why.

Honestly, a range — not a single number — and it's specific to your firm, not your industry's average. The useful version of the answer is built the way a buyer would build it: a defensible starting multiple, every headwind quantified in turns of EBITDA, and every value driver mapped to a repositioned ceiling. That's exactly what a complimentary read produces from public information alone — a starting point you can pressure-test before you ever talk to a buyer.

Want this run on your own firm? Get a read →

Operator

Jon spent over two decades as an executive of Afrocentric - a diversified investment holding firm - and as a strategy consultant. In that time, he reviewed several hundred private companies for acquisition. Most were rejected. The reasons were patterned and repeatable, and the patterns became the spine of a methodology for the owners on the other side of the table.

Multiple Forge is a practice dedicated to one question: how do owner-led services businesses become the kind of platform a strategic buyer pays a premium for? The buy-side lens is industry-agnostic; vertical-specific applications live under sibling sites.

The team-of-six analysis pyramid has been replaced by a methodology engine. Jon directs every engagement personally. The engine produces the artifacts - faster, cheaper, at consulting-grade quality.